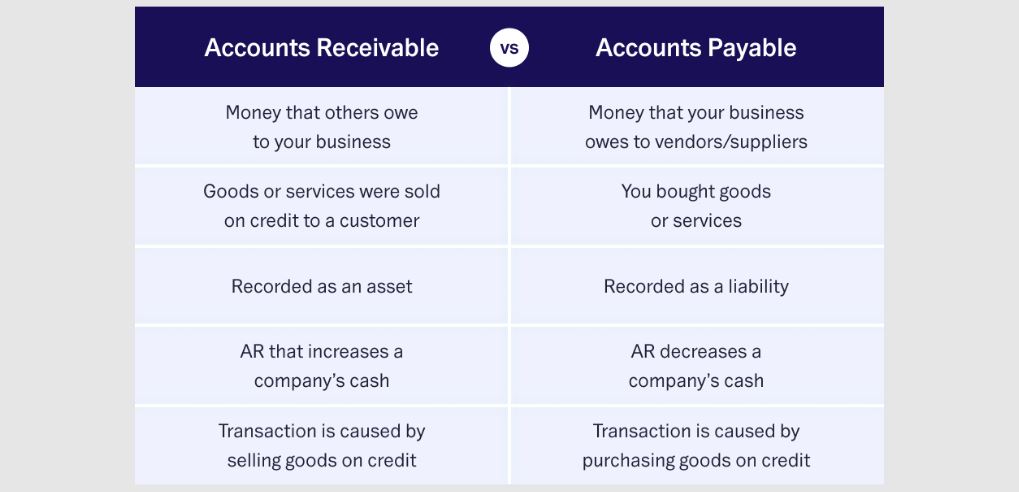

1. Accounts Payable

and Receivable

Accounts is the key information generator in any

commercial organization, it is the basic data recording technique that enables

decision makers to gain access to data that can be analysed on various

parameters and then utilized to as INFORMATION, and in order to do so the data

input method has to be not only error free but also needs to be a predefined

format to capture all aspects that shall translate it into a meaningful

arrangement that shall serve its purpose. And for same ABC3M shifts

focus from Financial Accounting to Cost Accounting or rather towards Management

Information System by use of Technique Manufacturing Accounting. Manufacturing

Accounting is tweaking financial accounting into more detailed accounting

process where each transaction recorded translates into information that can

provide details about Business Process relating to that transaction and records

not only the historic cost element but perpetuating effect and cause benefit

relationship behind decision pertaining to that transaction. For example when

Financial Accounts follows Historical Cost Method for Valuation of Inventory

(FIFO) the Manufacturing Accounting proposes to use Current Replacement Cost

and requires effects of same to be recorded into Books with immediate effect to

have clear Financial Understanding of Books, To illustrate further lets discuss

two sides of this transaction, If Goods are purchased on X day at Rs 100 and

Prices of same rise on X+1 Day by Rs 10 then Closing value of same on X+1 Day

will be Rs 110, but the unrealised profit of same has to be charged to Profit

and Loss Statement by reducing profit by Rs 10 and needs to be shown in books

of accounts as separate line Item as Unrealized gains. And here lies the

problem; Accounting Convention and Accounting Standard dictates that no such

Unrealized profit can be accounted unless there is certainty that such sale can

occur at Rs 110 and another important aspect AS 2 specifically requires that

Inventory has to be shown at Historic Cost or Market Value Which ever is Low

and the Profit has to be adjusted accordingly. Now management has to now its

capacity to generate money in near future by sale of such inventory and if they

see that less amount can be realized through Inventory Sale they might make

decision that can lead to wrong decision regarding Purchase or Production

Scheduling and for same they need to have details of Quantity, Quality and

Realizable Value of Inventory in hand. This is where Financial Accounting falls

short, as it provides information based on inputs and most of accountants

follow the data recording method derived from Accounting Standards they cannot

capture true incense information required by management,

Another Aspect is Record Keeping as per needs of regulators,

In our country Accounts are needs to be kept as per Business Requirements, also

as per Companies Act and also as Per Tax Accounting Standards, and Most of

Companies keep it as per Tax Accounting Standards to avoid duplication of work

and to avoid mismatching of data, This Leads to inadequate information for

Decision Makers as Data is not adequate to make decision, And of a Separate Set

of Data is needed to be maintained for Management Decision Making Purpose that

increases work load in all departments as well as increases work of

reconciliation between all departments and its validation through Accounts

Department.

ABC3M proposes to address this issue by simply

following Manufacturing Accounting as per Costing System of Company, This has

particular advantage of real time decision making matrix availability across

all functions as each function has to propose transactions as per there own set

of requirements they pass on information for to authorized person in the form

which allows its recording into a cost accounting record which also provides

recording of its impact into financial records as per needs of regulators like

Tax Authorities and others.

To Understand this in detail we are going to carry out

detailed questionnaire based on Accounting Standards linked with Costing to

help Accountants and Directors to understand the relationship between all

transactions and its impact and severity of impact on Key Aspects of

Profitability and other Decisions of Company like Capacity Building and Market

Share etc.

The Exercise will be first List of Transactions Covered into

Each Accounting Standard and the List of Decisions Linked with Transactions and

Requirements of MIS with that decision and how Manufacturing Accounting will

treat same and subsequent accounting treatments required for balancing the

Financial Accounts with Cost Accounting will be listed. This will also create

basis for catalysing BOD to understand key decisions to be made and there

frequency to enable them focus more on KEY BUSINESS OF COMPANY rather than desirable

aspects of running company.

Accounting Standard 1 Disclosure of Accounting Policies

This Standard deals with Selection of Accounting Method by

Company and Its Conformance with Generally Accepted Accounting Principles and

Conventions, As Most of the world requires a uniform method of accounting to

have clear understanding of performance and comparability between two similar

sets of information it requires the complete disclosure of method of accounting

selected and if there is any deviation from common practices that needs to be

disclosed separately so user of information can make his decisions based on

effects aroused due to such deviation and can understand more about the

company. Most of such deviations are covered in subsequent Accounting Standards

and hence we will revisit the AS1 again after completion of this part.

Accounting Standard 2 Inventory Valuation

In Operations of Company most significant operation is Sale

of Goods/ Services that translates into Monitory Rewards to Company, Hence to

achieve sale most important part is Actual Change of Hands of Goods/ Services

involved, And that means whole Value Addition Happens when actual movement of

Goods/ Services happen, thus it is important that this transaction shall happen

in most efficient way to achieve objectives of company i.e. Achieve Profit,

Increase Market Share, Develop Brand, Create Opportunity for Subsequent Sale,

Have long relationship with users, Create Value Proposition for User.

Now this Value Creation for User can be:

Cost Leadership, Perfect Operation, Reduction in Overall

Operating Cost, Display of Wealth, Completion of Desire, Projection of Might or

Simply Reduction in worry, And for same they have allowable Budget based on

Comparative Products, Replacement Products, Alternative Products or change in

Utility or reorganizing work flow or compromise and in any such aspect utmost

important factors are Price, Position, Utility, Timing, People, Place, Product

(7 P of Marketing) and then this leads to introspection of service provider – Goods

Supplier company and that translates into Decision relating to Inventory are:

·

Level of Inventory to be managed

·

Cost of Inventory Management

·

Valuation of Inventory

·

Working Capital Decisions Relating to Inventory

·

Effect of Inventory Management with Competition

Management

·

WIP Valuation for Operations Management

·

Production Scheduling and Inward Supply Chain

Management Linked with Inventory Position and Its Effect on Operations of

Company

·

Forward Contracts relating to Purchases and Sale

of Inventory particularly effects of Macro Economic Factors on Pricing and

Costing of Goods (inwards and Outwards)

·

Distribution and Sales Co-ordination relating to

movement of Inventory and Its Effect on Market Share

And To make all these decisions require information is Value

of Inventory, Potential Change in its Cost, Process Cost to Make goods ready

for Delivery (COGS) and Allocable Portion of OH in COGS and its Classification

and OH Absorption Method and Use of Marginal Cost Method for Making Relevant

Decision.

In order to gather this information accountant needs to

record all these elements in orderly manner to reflect all necessary data in

decision making matrix; making him service provider for all departments and to

achieve same he needs to use technique of Cost Accounting to ensure that all

relevant factors contributing to COGS are recorded at time of Transaction

itself, here we have to understand that it is not just Cost of Purchase and

Expenses Related to Bringing Goods into Factory are essential but also important

are the Expenses needed to convert those Inputs into Finished Goods and Hence

WIP becomes more significant.

In this Process often accountants are not keen on keeping

these records ready due to overlap of Accounting Function with Invoicing Work

and Other Statutory Record Keeping. ABC3M thus suggests to follow

Manufacturing Accounting for same. E.g.

The WIP Valuation is the area where often decision making is

difficult and to resolve same a simple step of Manufacturing Accounting can

solve same. The Transaction is Charging Production OH to WIP, In normal

Financial Accounting OH are charged to P&L Directly reducing the entry for

same, In Costing P&L however the Production OH is First Charged to

Production and then further Accounted for Product or Process.

Explanation:

Normal Accounting Entry:

P&L A/C Dr

To Party A/C

(Being Expenses Recorded for Production By Invoice Dated

--/00/0000)

Party A/C Dr

To Cash

A/C

(Being Cash Paid for Invoice Raised on --/00/000 as per

verification and Authorization done by BOD)

In Cost Accounting Entry:

Production Expenses Control A/C Dr

To

Party A/C

(Being Production Expenses Recorded authorized by Production

in-charge by way of Budgetory allocation under Doc No aa-bb dated 00/00/0000

and Invoiced raised as per PO no aa dated 00/00/0000 authorized by BOD as on

00/00/0000)

Batch xyz/ Product xyz/ Project xyz/ Service xyz A/C Dr

To

Production Expenses Control A/C

(Being Production Expenses charged to Batch/ Product/

Service as per report Submitted by Production In-charge as per Master

Production Schedule Dated 00/00/0000 authorized by BOD and Checked by

Functional Head Mr. xxx with Report of Consumption of Utilities and Inputs

bearing Doc no xx-xx dated 00/00/0000)

Party A/C Dr

To

Cash-Bank A/C

(Being Cash Paid to Party As per Terms of Payment with

Authorization from BOD dated 00/00/0000 bearing Transaction ID xxxx)

Now the Difference is Visible, If First Method Financial

Effect is Directly Visible and Useful when operations are small and Centralized

Payment exists with Very Few Entries to handle, But Situation Changes when

there are handful of Transactions Happening and it becomes more complicated

with Number of Inputs Increases with Complexity of Parts and Number of People

Handling Goods and Even more complexity happens when there are more than 1

Vendor for Each Product and also when there is no standard Product is offered

and each Good/ Service Sold is a variation. In such scenario no Information is

available to BOD in relation to effective use to particular Input which can be

traced backed to Output of Firm and to solve same ABC3M asks

Accountants to get in touch with production rather than with Financial

Statements. The reason for same is quite simple Accounting is RECORDING OF DATA

not DECISION MAKING, DECISION MAKING is Functional Heads responsibility and for

them Accounts is Service Provider and This Service Provider can help best when

Functional Heads Communicate information regarding operations with relevant

Authorizations and in orderly manner with predefined rules to accounts to

seamless transaction processing.

The BOD in turn can have real time information or at least

at every day end the clear financial Position of Company with clarity about

what work priority can be adhere to.

Now the Accounting Part, This Cost Accounting Approach also

effects the Valuation of Inventory, With This Production Expenses Control

Account and Product/Service/ Batch Account the Position of Valuation of WIP is

Clear as Instead of Charging Expenses to P&L now it Direct gets Charged to

relevant Product/ Service and The WIP Valuation is Real, If The Market

Realization Value of WIP at reporting period is Less Than Cost Incurred then it

Can Be Charged to Costing P&L and If Market Realization Value is more then

as per Accounting Conventions the Unrealized Profit is Not recorded at all,

Apart From that The Balance in Production Expenses Control Account Can be

Directly Charged to Costing P&L Reflecting Actual Profit- Loss Position of

Company for Reporting Period (The Balance in Production Control Account

represents Under Absorbed or Over Absorbed OH Amount that needs to be adjusted

for Reporting Period)

This Increases work in Accounting Function but reduces lots

of Waste of Resources in Value Driving Functions as to make it effective clear,

error free and Formatted Data has to be exchanged it triggers Controls and

Observations at each step creating a Log of Information and Authorization

before recording, It also Provides Real time Performance Measurement of respective

department and helps Functional Heads to make Prompt Actions, And Utmost

Important Benefit is reduced Time for Individuals regarding Data Input as

instead of providing unstructured Data they need to fill up only those details

that are necessary for there respective work. This also helps increased

Aggregate Efficiency and Productivity as Incentives are linked with overall

performance rather than individual performance and also requires BOD to Provide

stream lined Activity Schedule forcing them to pay attention to Bottleneck

areas and focus more on people who can perform and make necessary decisions.

Keeping the same principle when Each Expenses Item is

segregated into Cost Centre and then Charging Method is adopted (Control

Account is Created) then the process becomes more effective and helps Functional

Heads to keep track of Operations rather than worrying about recording of

various information.

Accounting Standard 3 Cash Flow Statements

AS 3 Deals Mainly with 3 Aspects of Business:

Cash flow From Operating Activities

Cash Flow from Investing Activities &

Cash Flow from Financing Activities

It also pay attention related to FOREX Transactions and

Extra ordinary Items, Dividends and Taxes as they represent stake holders

interest points with regards to Validation of Financial Position in Real Cash

Basis.

The Line Items of these Cash Flow Statements are Pure Cash

Outcome of All Decisions made by Executives of Company and can be seen in Money

Value by any person carrying commerce

The Items of same represent Following Transactions:

Operating Activities

Cash flows from operating activities are primarily derived

from the principal revenue-producing activities of the enterprise. Therefore,

they generally result from the transactions and other events that enter into

the determination of net profit or loss. Examples of cash flows from operating activities

are:

(a) cash

receipts from the sale of goods and the rendering of services;

(b) cash

receipts from royalties, fees, commissions and other revenue;

(c) cash payments

to suppliers for goods and services;

(d) cash

payments to and on behalf of employees;

(e) cash

receipts and cash payments of an insurance enterprise for premiums and claims,

annuities and other policy benefits;

(f) cash

payments or refunds of income taxes unless they can be specifically identified

with financing and investing activities; and Cash Flow Statements

(g) cash

receipts and payments relating to futures contracts, forward contracts, option

contracts and swap contracts when the contracts are held for dealing or trading

purposes.

Investing Activities

The separate disclosure of cash flows arising from investing

activities is important because the cash flows represent the extent to which

expenditures have been made for resources intended to generate future income

and cash flows. Examples of cash flows arising from investing activities are:

(a) cash

payments to acquire fixed assets (including intangibles). These payments

include those relating to capitalised research and development costs and self-constructed

fixed assets;

(b) cash

receipts from disposal of fixed assets (including intangibles);

(c) cash

payments to acquire shares, warrants or debt instruments of other enterprises

and interests in joint ventures (other than payments for those instruments

considered to be cash equivalents

and those

held for dealing or trading purposes);

(d) cash

receipts from disposal of shares, warrants or debt instruments of other

enterprises and interests in joint ventures (other than receipts from those

instruments considered to be cash equivalents and those held for dealing or

trading purposes);

(e) cash

advances and loans made to third parties (other than advances and loans made by

a financial enterprise);

(f) cash

receipts from the repayment of advances and loans made to third parties (other

than advances and loans of a financial enterprise);

(g) cash

payments for futures contracts, forward contracts, option contracts and swap

contracts except when the contracts are held for dealing or trading purposes,

or the payments are classified as

financing

activities; and

(h) cash

receipts from futures contracts, forward contracts, option contracts and swap

contracts except when the contracts are held for dealing or trading purposes,

or the receipts are classified as

financing activities.

Financing Activities

The separate disclosure of cash flows arising from financing

activities is important because it is useful in predicting claims on future

cash flows by providers of funds (both capital and borrowings) to the enterprise.

Examples of cash flows arising from financing activities are:

(a) cash

proceeds from issuing shares or other similar instruments;

(b) cash

proceeds from issuing debentures, loans, notes, bonds, and other short or

long-term borrowings; and

(c) cash

repayments of amounts borrowed.

If we read

each line Item, it is essential a Business Decision Relating to Either

Operations or Financial Planning, The FINANCFE Function is more concerned with

same as it expects the Finance to have role in making decisions but again is a

Client of Accounts and Accounts needs to record all these transactions in

manner that the real time use of relevant information can be made, And ABC3M

Suggests that each Transaction listed above relates to a Particular Function

and VALUE ANALYSIS AND PLANNING FOR ACHIVING SAME shall be done by respective

Functional/ Departmental Head and Authorization Resource Allocation shall be

done by Finance Department for same only after Priority List is Prepared by BOD

within limitation of Resources. And Accounts shall Provide Comparable data of

Past Performance and Overlapping or Existing Resources for same through

Manufacturing Accounting, For Example In Financing Decision key aspects are

Benefits arising from use of Asset, Its ROI, Sunk Cost Due change in Operations

or Use, Cost of Finance (Equity and Debt) Alternative Use of Asset and

Available Alternatives of Asset are key decisions, Functional Heads can make

decision about these aspects but the past data of such advantage or effective

use of prior assets can be easily identified with Track of Depreciation and

Amortization Charts if they are maintained in orderly manner, it will also help

to find weight in Claim of Functional Head if he had performed in past with

similar acquisition of asset and its use, it will also help keep track of

Finance Cost that also Forms part of COGS as Line Item Before Selling And

Distribution Cost. This also effects Linkage between Charge of Fixed Asset

Investment on Overall Cost and Marginal Cost Per Unit of Output.

The Mistake

made by BOD is often Not Considering the Overall Effect on Cash flow due to

Availability or Non Availability of Assets as well as Alternative Financing

Arrangement, For Example If Particular asset is outside of Financial Capacity

of Firm but it can build good work load for same assets it can simply have

Joint Venture with another firm for Sharing the Asset, its Advantages and Also

make decision about Risk Sharing Arrangement, But do so Company requires

internal assessment of Cost Benefits and for same it needs Work Load

calculation and also inputs like Working Capital Constraints and Cost of

Capital and Inventory Turnover Ratio etc inputs, A Right Manufacturing

Accounting Process will Provide basic Data in more relevant manner for same if

designed in way the Firm has phases of Business operations Planned. ABC3M

again brings back BOD to Planning Board where they have to dive into PLC and

Industry Analysis to have opportunities validated and primary operations

drafted to revisit them at each periodic instance to validate and updates as

per dynamics of Business Environment and for same Accountants are required to

provide data on Cash Generated through Operations.

There are

other implications of same as well, Financial Profit considers Unearned Cash

through Debtors Position but ignores the fact that some of them may be

irrecoverable, It requires provision to be made with reasonable assumption but

again it is deductible in eyes of tax man becomes subjective matter, on other

hand Carry forward of Provisions and Unsettled accounts also creates problems

at it is reflected in Opening and Closing Balances as well giving falls

impression of healthy operations, Thus More relevant information is about their

recoverability and Costs related to their recovery as well as position in books

(Finance Cost related to delayed recovery) this is not accurately MAPPED in

Financial Accounts in straight forward reading as notes forming part of

accounts are vague on many aspects of transactions and often ignored, also the newer

disclosure requirements are not intuitive for reading.

The BOD then

have to rely on information that is not 100% Reliable and also needs further

details before decisions, Again the External Stake Holders Like bank and

Financiers require further details for overall analysis which is called CMA

Data and Concise Version of Cost Sheet linked with Financial Accounts i.e.

Manufacturing Accounts. And as per experience with SME they need to create same

every time they are opting for CC Renewal or Machine Financing, This Further

Establishes the requirement of more detailed Accounting Information

(Financials) in Cost Sheet Based Data which ABC3M proposes to be

recorded in real time to become control tool rather than Compliance.

The Extra

ordinary Items in AS 3 are related to Accidents, Unplanned Events and

unanticipated transactions are to be disclosed by Management at each Financial

Reporting Period (Quarterly and Annually) they represent the ability of Company

to Cope up with Environment thus needs to be first recorded in manner that

reflects true capacity of company, For Example if Flood interrupts production

12 days resulting very low inventory position at end of reporting period, it is

not fault of SCM in Inventory Management and Safety Stocks can not be increased

based on single incidence, but it needs to be Diversified at various location

to systematically reduce target cost and maintain adaptability in Supply Chain,

Its Financial Position Implication that not enough Value is Created in End of

Period is also not proper presentation of capacity of Company and definitely is

not valid argument that company is loosing sale. The separate disclosure of

same can present this fact but to substantiate that claim records also must

provide detailed information about turnaround time taken by Operations and

Working Capital Movement in same period and Creditors Movement in subsequent

period also needs details of Debtors Position and Cash Recovery Rate pertaining

to post flood period, The Financial Accounting Data Provides this information

but in Unstructured manner, This may helpful to external readers but for BOD

and Investors key information is Hidden in form of Ledgers and Journals which

becomes hampering work, That can be eased with simple tool of Cost Accounting

linked with CRM to explain real time operations position that translates into a

Decision Making Matrix by way of Inputs from MIS rather than from Assumptions

and Unstructured Information.

Accounting Standard 4 Contingencies and Events Accruing

after Balance sheet Date

The AS4 Deals with primarily transactions that

do not complete within Time Limits of Reporting Period under consideration but

before actual reporting of same, For Example A Debtors goes Bankrupt after 31st

March but reporting is to be done on 1st May then in Books It

appears as favourable position to company but in reality that Loss Needs to be

corrected in Books, This laps in record keeping is acceptable when Company has

no knowledge of it, but if company has knowledge but does not report same, then

it is a problem, another aspect of same is that if company does not tracks such

events then it is a larger problem for company because Transaction Covered

under AS 4 are as Follows:

·

Contingent Losses on account of Debtors

Insolvency

·

Contingent Losses on Account of Changes in Tax

Structure

·

Penalties

·

Warranty Expenses

·

Loss of Assets in Accidents and Unforeseen

Incidences

·

Liabilities arising due to uncontrollable events

·

Recovery of Past Losses

·

Errors in Judgement or Estimation of Effects of

Past Transactions

·

Escalation Clauses in Contracts – Favourable or

Unfavourable

·

Employee Benefits related Calculations and

Allocations

·

Change is Usefulness of Asset

As This List is not Exhaustive neither it can be said to be

completed and applicable to each Firm with same degree of relation, ABC3M

takes approach of Preventive planning in same and in partnership with each

Functional Head it prepares a list of possible occurrences and then requires

Directors to prepare a monitoring Matrix which helps Functional Heads to Prepare

a watch list in line with ABC Technique used in Inventory Management to ensure

that Key aspects are monitored regularly to Make Post Effect Decisions more

smoothly and Help Finance Department to keep adequate Cash Ready to manage Risk

of Interruption and also Arrive at SAFTY CAPITAL and Charge of its Cost

to overall operations, this also keep BOD informed about Week Points in System

to keep watch at. And for same ABC3M again asks BOD to Scan Business

Environment to carry out Risk Profiling on each aspect of Business and then

make Strategy Based on Constraints of Resources.

The undiscussed Item in this Analysis is the Joint Ventures

and Commercial Arrangements and their implications on main business also needs

to paid attention to, The Formal Arrangement may not exist between Upward and

Downward Supply Chain but often Businesses make investments in SCM in Vertical

and Lateral direction in guise of

Businesses Leniency and Commercial Relationship, But with time and Dynamics

these relationships are often not monitored as they are non-core activities for

Business and thus there direct link is not disclosed but are they are a Direct

Force Effecting the Operations, and the shocks of such change are not affected

in Financial Position, But as Decision Makers BOD must understand its complex

effects on Organization and thus needs to reported, But no such formal

Accounting convention exists apart from Disclosure Requirements, And to improve

upon same if Functional Heads Dealing with such parties make it part of their

reporting it makes easy to take care of same, Again this needs to paid

attention to as per Needs of Organization and Cost Accounting System

Accommodates such requirement by Way of 2 Tools Control Accounts and

Provisions, And streamlines Financial Accounting and Tax Accounting BY Way of

Reconciliation Entries in real time.

Accounting Standard 5 Net Profit and Loss for Period and

Prior Period Items and Changes in Accounting Policies

This AS deals with Transactions that are Regular,

Extraordinary and Not related to current period and Specifically Changes in

Accounting Methods, We need to pay attention to Disclosure requirements and

other aspects are already discussed while discussing AS 4, The Main aspect that

needs to observe here is Changes in Accounting Policies, The most of Accounting

Frauds are done with allowed Freedom for deviation or change from regular

methods of accounting and policies and also changes in presenting facts, E.g.

Diff rate for Charging Depreciation or Changing accounting from Cash Basis to

Accrual Basis or change in Accounting Period. For External Parties the relevant

information is catered through Financial Accounts but for MIS Purpose necessary

changes in Practice are crucial as the Method of Costing can not be same for

each Company and More Importantly Within Company Itself A Different Method of

Costing needs to be followed to Make right Decisions and that may not be in

line with regulators perspective or simply not required, But the Estimation and

Absorption Methods of Cost and Revenue Items Differs on Actual Basis, this

gives conflict with regulators inviting scruitiny, And to tackle same ABC3M

has to have Balancing Accounting Steps as Check Bits and Reconciliation Points

that has to be Periodically Matched with Overall Data and Hence Accounts have

to get in shoes of Financial Controller and then translate its process to

ensure overall compliances. When the Calendar is set for such Transaction

Recording and Verification it reduces need to Scruitiny by BOD and Allows BOD

to Pursue More Important tasks of company that drive main objectives of

company.

Accounting Standard 7 Construction Contracts

AS 7 Mainly Deals with:

COMBINING

AND SEGMENTING CONSTRUCTION CONTRACTS

CONTRACT

REVENUE

CONTRACT

COSTS

RECOGNITION

OF CONTRACT REVENUE AND EXPENSES

RECOGNITION

OF EXPECTED LOSSES

CHANGES IN

ESTIMATES

DISCLOSURE

REQUIRMENTS

As a Company

it may be a Contractor or Client depending upon Nature of Transaction

When Company

is Contractor it has pay attention to Revenue, Costs and Value Addition/ Loss

from Transaction and When Company is Recipient then it has to pay attention to

escalation clauses, Conformity with Contracted Benefits, Quality Delivery,

Timely Completion and Effects due to Non-Timely Work and Errors in Execution

and Unaccepted circumstances.

Again, when

Construction Contracts are drafted all such criterion are mate when both

parties experience in same and fully aware of aspects that can hinder actual

work and consequences of same there are very less instances of friction, But

when parties involved are ill prepared and liability clauses are drafted

without due consideration to variable factors then it makes difficult to

execute work and also keep costs in control.

As Basic

Principle of ABC3M is Identify Requirement First, Plan Within

bounds, Engage Domain Experts and then execute it simply reduces overall lag

and friction in work,

The

Accountants role in same becomes as Valuer of Work being done, Financial

Controller for Transaction Processing and Pre-Payment Authorization and Recording

of Transactions in Manner required by organization by rules of Cost Accounting.

It even makes Inter Firm Communication clear to oversea the execution more

smoothly with accuracy and in real time.

To Enable so

ABC3M suggest using Project Costing Method with Use of OH Accounting

on the basis suitable for Company, It can be Man Hours, Actual Accounting or

any other Cost Driver based on actual terms of Contract.

Illustration:

When A Ltd

Contracts with B Ltd to Build a Silo in Company Premise and to control cost

provides in house engineer for overseeing work, Then Cost Of Asset also needs

to include Cost of Engineers time spent on that job, But That Salary is Revenue

Item for Company which can get charged Double as expenses in Salary and Again

Accounted Twice as Cost of Asset, This has Tax Implication as well, As Revenue

Expenditure is tax Deductible expenses for Current period and If Charged to

Asset it is Depreciated over useful life of Asset.

Now for Tax

Purpose it is Beneficial to Charge Engineers cost to Revenue but for MIS

Purpose that expenses is essential for making replacement decision and cost

advantage analysis to compare with competitors again that decision it self can

be of no use as Cost Asset being Sunk Cost when Decision is made with Principle

of Marginal Cost. But BOD Need Data to reflect that fact. When Sum Involved is

insignificant then it can be simply ignored but consider a scenario when Such

Asset is built with External Financing and Company is able to save Direct Cash

Flow; at cost of Deviation of Regular Business Activities towards asset

construction then this all becomes signification, We also have to consider this

with aspect when company is Provider of Infrastructure goods/ services it has

to understand clients perspective to present commercial terms and take

advantage of situation by staying more informed and enhanced user profiling to

bag more and more orders. The ABC3M in this Scenario will help

company to identify trends in User Profile itself and when Value Proposition

Statement is Prepared it will allow the company to take position in way that it

will allow to have more impact to client than competitors. Again, Accountants

can serve as Input Providers in all such process to increase value of company.

The Next

Aspect under consideration is Costs associated with Construction Contracts and Sharing

of same on Contingency Clauses, A Good accountant will always monitor all cost

elements at time of recording of expenses and revenue itself and help

Functional Heads to make aware about performance of such job and also help them

identify Indirect Costs like Cost of Finance, S&D and Admin OH to make

decisions within framework of allowable scope of work, or allow Site in-charge

to make addition expenses who’s Value in terms of Tangible and Non Tangible

Benefits will be more. Allowing Company to make impact in Market in terms of

Brand, Distinctive Identity and Driver od Excellence.

Recognition

of Expected Losses: Often Businesses undertake some job for reasons like

fending off competition or Market Share Maintenance and Cross Selling

Opportunities, In Such cases it needs to be reflected in not just MIS but in

Financial Accounts as well as this is utmost important factor for External

Stakeholders to judge the true capacity and market position of company, ABC3M

requires Accountants to Treat All Such Instances as Separate Line Item and a

Disclosure of same is to be made in line with AS3 AS4 and AS7. Often Such losses can be recouped with

further extension of contract or increased scope of work and this needs to

reported on individual and aggregate level to ensure true position is disclosed

and BOD can understand Opportunities Available and Long Term Impact of Such

Transaction enabling them to steer company in more efficiently.

Accounting Standard 9 Revenue Recognition

This AS deals with methods for Revenue Recording

based of Direct Operating Activities and Revenue Earned through Letting others

use resources of Company. Aspects Dealt in same are:

·

Revenue earned through Sale of Goods/ Services

·

Activities Covered over more than 1 Period of

Time

·

Uncertainties Pertaining to Unearned Revenue and

Contingent Losses

·

Royalties and Other Incomes based on Tangible

and Non-Tangible assets of Company

·

Treatment of Interest and Dividend Incomes

·

Deduction of Taxes from Revenue

·

Sale

achieved through Installments and Linked Services and Matching Principle

relating to Revenue Recognition

ABC3M adds value in same only by adding more check points of Procedural Aspects, The AS is self-explanatory about Principles of Revenue Recognition but often it is observed that lack of training in Accountant increases risk in this aspect when they fail to establish the fact that EEESNTIAL LIABILITIES AND OWNERSHIP RELATING TO GOODS/ SERVICES UNDER CONSIDERATION can be established by way